Nestegg Cycle © How to Actually Engineer a "4% Rule" Retirement (Part 2)

Posting Date: May 19, 2022Why we noted in Part1 that the 4.0% withdrawal rate was for the first year only, and what happens afterward.

First, we want to point out a number of distinctions between NesteggCycle's calculations and

the original "4% Rule" concept as developed by Bill Bengen in 1994 .

Mr. Bengen's focus involved statistical analysis of historical records of investment market performance and probabilities of success,

which applied specifically to a 30-year retirement, with a portfolio evenly split between stocks and bonds.

The finding, simplified here, was that if a retiree withdrew exactly 4% of his/her retirement savings in the first year,

and adjusted the withdrawal for inflation each year after that,

it was a statistically strong bet that the money would survive a 30 year retirement,

and that in many cases, the money would have survived a 50 year retirement.

But be aware: "Past performance is NOT a guarantee of future results".

This "rule" is widely discussed and provides a useful and important perspective. It is by no means, a law of nature.

Here at NesteggCycle.com, the focus is straight math and no history.

We look at the same overall subject matter from a different angle.

Our calculations show the minimal conditions for a retirement scenario to succeed,

which means presenting calculated pay-in requirements during working years,

generating the necessary capacity to make all the required payouts over the term of years specified

(not necessarily thirty, and probably more, since our default retirement runs for 38 years)

and running the nestegg account down to a zero balance at that exact end point.

Nothing is said, nor implied, about the choice of stocks, bonds, nor any other investment vehicle,

but only hypothetically, what is the minimum investment yield required to succeed

under a variety of salary contribution conditions.

An observation which I believe to be interesting and important, is that over time,

the withdrawal ratio must naturally INCREASE as the nestegg depletes.

Thus, it is usually not possible to stick with a fixed withdrawal ratio though a whole retirement.

I think it is easy to assume that this ratio, be it 4% or any other, should be adhered-to

long term. This is not possible, and I will explore this phenomenon here. This can NOT be your compass.

We can analyze the life-cycle of retirement payouts, as an annuity, like a mortgage in reverse.

[ There are arguments as to whether this is the best we can do. See, for instance, HERE. ]

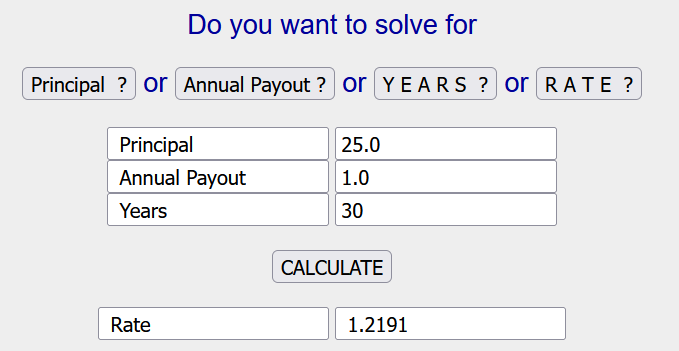

To replicate Bengen's "4%" scenario over 30 years,

and starting with a nestegg containing 25 times the initial payout (since this is the same as taking 4%)

We can use an annuity calculator site such as this one , and solve for the RATE,

which tells us that the investment yield required to maintain the payouts for exactly 30 years, is 1.2191%.

If there is inflation, this RATE must be adjusted to account for it, since the retiree is expecting COLA's.

Assuming inflation of 2.5% as we have throughout this discussion,

anything that costs 1.00 now, will cost 1.025 in one year.

Similarly, any 1.00 invested at 1.2191% will grow to 1.012191 in one year.

Multiplying these, we arrive at a required average investment yield of 3.75%.

1.025 * 1.012191 = 1.037496

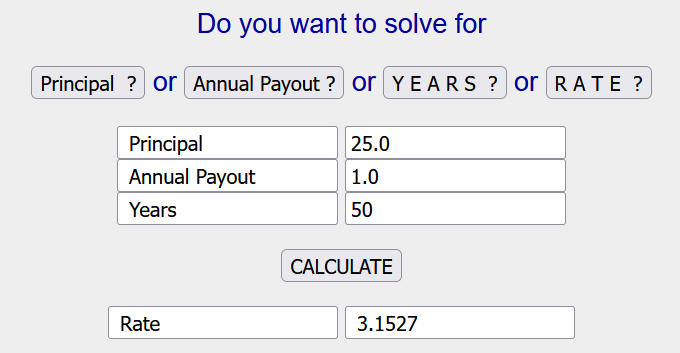

As mentioned earlier, the investment markets historically were sometimes strong enough to keep this nestegg solvent for 50 years, for which:

the performance bar was significantly higher - a pre-inflation average yield of 3.1527%. The inflation adjustment is:

1.025 * 1.031527 = 1.057315 ... THUS: 5.73% is the required average yield,

to overcome 2.5% inflation, and make retirement payouts for 50 years.

Having presented all of the above to set the stage, we are now almost ready to follow what happens to the withdrawal ratio during the normal life cycle of a retirement nestegg.

A final puzzle piece is how to determine the "remaining balance" of the nestegg at any time into the retirement payouts.

HERE is a suitable calculator I found for these calculations.

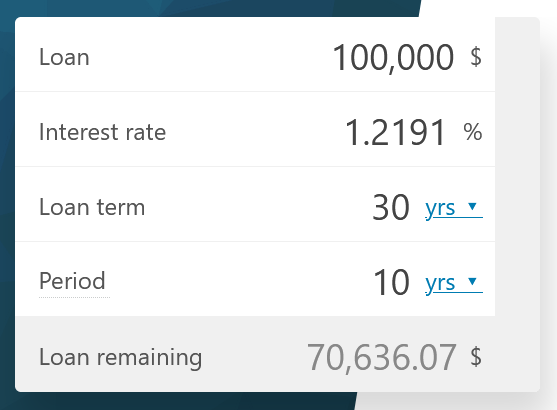

In the illustration just below, we see the calculation for 10 years into a 30 year retirement:

We want to know the percentage remaining, of the nestegg compared to the beginning of retirement,

and we are likening this to the starting balance of a loan.

To keep the math simple, we'll make the initial amount, a one followed by any reasonable number of zeroes.

We've used 100,000 but 1000 would have been fine also.

The "Loan remaining" is 70,636.07, so our percentage remaining is that over the 100,000 or 70.636%.

The choice of "Interest rate" to enter, is crucial for getting this right. For today's purpose, we need the rate that will keep the nestegg solvent for exactly 30 years, given the 4% payout in the first year, and we do NOT want any inflation adjustment. From the annuity calculation for 30 years, above, the Rate was 1.2191%. That is what we want. IF we only knew the inflation-adjusted rate, we would need to "DEFLATE" it now, reducing it by the inflation rate of 2.5%.

This also means that the interest rate we need for determining the remaining balance,

is different for each choice of retirement term, and best handled with the annuity calculator.

So finally, in the table below, we show the remaining balance at 10, 20, and 30 years into "4% Rule" retirements of varying TERMS, and show how this impacts the withdrawal ratio over time:

INITIAL withdrawal is always 4% of initial Principal, BUT what happens to that withdrawal rate over time? Inflation of 2.5% has been assumed: PAYOUT INCREASES by 2.5% each year. Use annuity calc: PRINC=25.0, PAYOUT=1.0 solve for DEFLATED-RATE at each TERM (years). RB (as in 10y-RB%) is the Remaining Balance percentage of the at-retirement Nestegg WR (as in 10y-WR%) is the Withdrawal Rate at this point (here, 10 years into the retirement) RATE DEFLATED TERM 10y-RB% 10y-WR% 20y-RB% 20y-WR% 30y-RB% 30y-WR% 6.60% 4.00% 200+ 100% 4.0% 100% 4.0% 100% 4.0% 6.3401% 3.7464% 75 97.08 4.120 92.84 4.308 86.66 4.616 5.7315% 3.1527% 50 90.33 4.428 77.08 5.189 58.93 6.788 4.8961% 2.3377% 38 81.59 4.903 58.34 6.856 28.97 13.807 3.750% 1.2191% 30 70.64 5.663 37.47 10.675 0.00 100.0

IF you had a compelling interest in keeping the withdrawal rate stable, you would need to work with a retirement term on the order of 75 years.

To support this, the retirement nestegg would need to earn at least 6.34% (3.75% before allowing for inflation).

Under these conditions, the 4% initial ratio rises to only 4.12% in ten years, 4.31% in 20, so you'd probably be OK for 10 years or so, using the approximation that it was a constant 4%.

For a 30 year term, the 4% withdrawal ratio grows considerably faster, to 5.663% at 10 years, to 10.675% at 20 years, and to 100% with the final payment at 30 years.

Our main focus at NesteggCycle.com, is how to build up a nestegg of suitable size. The simple payout model assumed here, is that your first year's retirement payment is 4% of initial nestegg, followed by an inflation adjustment to that amount in each succeeding year.

Out in the real world, where your nestegg's value does not follow a smooth path, but rather can have sharp jolts up or down in some years, there are extra steps to be taken to adjust the payouts. This is beyond the scope of our site, but there is plenty of material to be found if curious.

So what can be used as a "compass" to determine whether we're on track and make mid-course corrections?

Tracking progress during accumulation (BEFORE retirement):

Good topic for a possible future blog posting. General idea would be to compare your old NesteggCycle calculations, from perhaps two or three years ago, with your new current calculations including hopefully, the larger balance in your nestegg account, and determine whether the contributions and investment yield you selected back then, still work. This would be of interest to any retirement saver, 4% Rule or not. There may be some special extra steps to get this right when using any "X% Rule".

Tracking progress during payout (AFTER retirement):

If you've used the NesteggCycle software, you have an idea of how many years you want the nestegg to last before running out of money.

The default is 38 years (ages 67 to 105). For an early retirement, this term could be decades longer.

You must decide, for your own situation, how many years of payouts you need, and record the year and age that marks the end-point.

At any time, you can use the annuity calculator again.

You will know your current account balance (Principal) and the number of expected Years remaining for your payouts.

Annuity calculations to try:

Enter Principal and Years, then the annual payout amount you currently expect. Solve for the RATE, and see if that figure agrees with what your money is earning, and can reasonably continue to earn.

Another: supply an interest rate, and solve for the annual PAYOUT.

Another: supply an interest rate and payout, and solve for TERM: how many years of payouts, this would provide.

For each calculation, try a range of values to get a sense of what's too high, about right, and too low.

All calculations need to be adjusted for the amount of inflation you assume. The inflation adjustment was explained above, within this article. You'll quickly see whether payout adjustments are warranted, and in which direction.

You may wish to discuss these findings with a trusted advisor.