Nestegg Cycle © SPENDING POWER:

For enough background, please be sure you have read "SET YOUR GOAL",

especially the section, "DISCUSSION of Spending Power Adjustment"

Beginning with version 2.1, introduced in early May of 2022,

the Adjustment for Spending Power has new capability.

Previously, it was inert, and simply there as an alternative choice.

Now, some new things happen: The label content is dynamic, showing your spending power at retirement

in numerical relation to your spending power when you started working. The wording changes to show whether your

spending power has INcreased or DEcreased. Finally, when this is deemed worthy of being called to your

attention, the label is high-lited with an eye-catching yellow background.

Your spending power is in a tug-of-war between your salary raises, and the general inflation of prices.

IF your raises are larger than the inflation rate, your spending power GROWS, and will have a value GREATER than 1.000

And because of your INcreased spending power, your desired retirement PAYOUT can be satisfied with a

SMALLER-than-GOAL percentage of final salary,

and this is shown as the Adjustment for Spending Power.

Whereas ...

IF inflation is larger than your salary raises, your spending power SHRINKS, and will have a value LESS than 1.000

And because of your DEcreased spending power, your desired retirement PAYOUT will require a

LARGER-than-GOAL percentage of final salary,

and this is shown as the Adjustment for Spending Power.

Either way, the effect (which might not be noticeable in one year) is magnified by time. That is the power of compounding.

When you see that the Adjusted Spending Power label is high-lighted in yellow, you are STRONGLY URGED to select this

by clicking on its radio button, which will cause the CALCULATION of contribution/yield pairs, to be based on the Adjusted Goal.

Demonstration of how your inputs affect your spending power calculation:

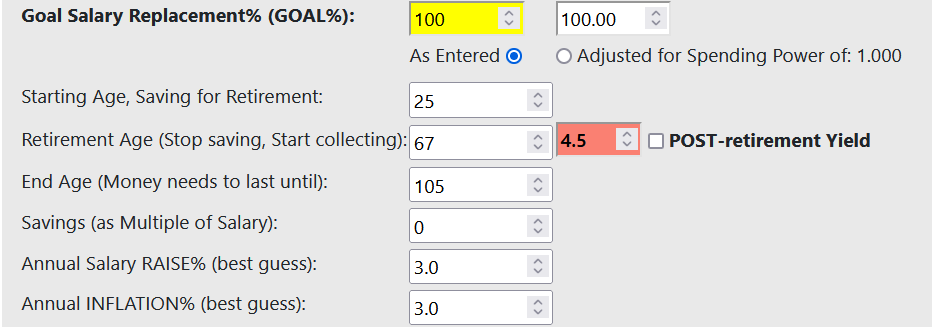

To set this up, first make a note of the GOAL% you were using, then change this to 100% on the screen.

Next, note the Raise and Inflation you wanted to use, then change BOTH to 3.0%.

Keep the starting and retirement ages at 25 and 67, so that you get the same amount of compounding,

42 years, shown here.

The spending power adjustments are recalculated immediately, as soon as your mouse exits from a changed

data entry box.

Thus you will NOT need to click on the CALCULATE button at all, while working thru this demonstration.

The initial setup (3% and 3%) gives an Adjusted Goal of 100% -- SAME as the original Goal. Spending Power is 1.000

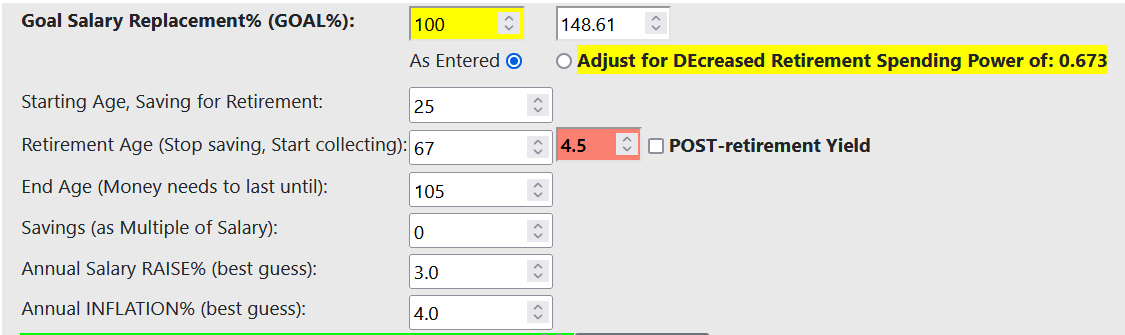

Keeping the Raise at 3%, change the inflation to 4%, to demonstrate SHRINKING spending power:

We get: Adjusted Goal = 148.61%; Spending Power of: 0.673

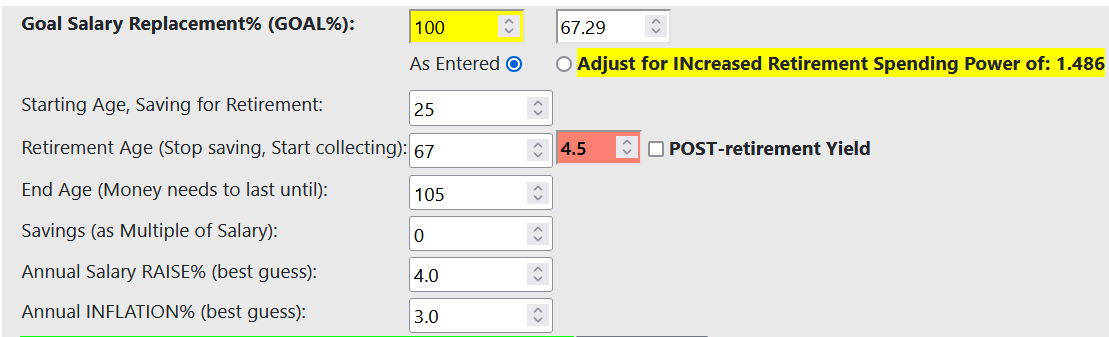

Reverse these to Raise of 4% and Inflation of 3%, to demonstrate GROWING spending power:

Now we get: Adjusted Goal = 67.29%; Spending Power of: 1.486

Useful Fact: the product, (Adjusted Goal) x (Spending Power), always equals the original Goal (here, 100%).

Because I set the Goal to 100% for both GROWING and SHRINKING, it is a bit easier to grasp the relative numbers;

How much do we need to care about Spending Power?

In the above demo, the inflation rate and your raises were similar.

But what would things look like, if you had an extended period of higher inflation during your working career?

Let's step through a series of increasing inflation rates while holding raises constant at 3%, and chart the effect on spending power.

We already worked 4% inflation. Now we add a row for 2%, then step through 6%, 8%, 10% and 12%.

Inflation Spending_Power 2% 1.492 4% 0.673 6% 0.308 8% 0.143 10% 0.067 12% 0.032

Your retirement spending power would shrink horribly and the Adjusted GOAL would become correspondingly unworkable.

This is so, because the mathematically correct adjustments would come to require unaffordably high salary contributions and at the same time,

unattainably high investment yield requirements.

We've used a GOAL% replacement of 100% for illustration in this demo.

A more "typical" goal might be 50%, assuming that you would have access to other income streams such as a government pension.

The "right" goal depends on your personal circumstances.

Under the stress of 10% inflation, the contributions that you intended to satisfy a 50% GOAL, would only provide 0.067 x 50%, or 3.35% salary replacement in real terms.

To keep this discussion fair, note that these calculations assumed annual salary raises of 3% and are sensitive to the size of the raises you specify. Had there been no raises, or larger raises, then 10% inflation would have had very different impacts.

Think of it this way: Suppose you start working in 2022, earning, say, $5000 per month. You plan to make contributions to fund a 50% retirement, and you have a sense of what that 50% (2500 per month) would buy, in 2022. But after 42 years at 10% inflation, although you'd have the number of dollars you intended, you'd only have the spending power of 0.067 x $2500, or $167.50 per month (in year-2022 terms).

Without supplementary income streams to make up the difference, you would be drastically short of what you'd planned and expected.

Your remedies would include efforts to raise your salary faster, efforts to make do with less,

efforts to find higher-yielding investments, and probably, a lowering of expectations -- a lowered retirement GOAL%.