Nestegg Cycle © Save 2X Salary by Age 35? How to, and Whether to

Posting Date: June 25, 2022A few years back, Fidelity Investments created quite a flap by publishing an article, how-much-money-do-i-need-to-retire

which included a set of "milestones" toward retirement, in the form of a table showing how much savings you should try to accumulate by each 5-years of age. In particular, their recommendation for age 35, assumed to be 10 years into your accumulation, was DOUBLE your age-35 salary.

Readers will want to study Fidelity's extensive footnotes, which explain their methodology and assumptions.

In this posting, we intend to cover:

0 - Site Concepts, Ground Rules, and Operations,

1 - Broad-range Survey of Retirement Solutions using Fidelity's assumptions,

2 - What it Will Actually Take to REACH 2X Salary Saved by Age 35,

3 - Why you MIGHT WANT to save 2X Salary OR MORE by Age 35,

Why you MIGHT NOT NEED TO,

and Why the 2X milestone for age-35 is essentially meaningless!

0: Site Concepts, Ground Rules, and Operations

This site performs a mathematical analysis you've not seen anywhere else.Each row of the on-screen results table, is a valid solution to the proposed retirement.

Each solution is a Salary Contribution, paired with an Investment Yield; each is an accurate depiction of alternative minimum conditions that WOULD NEED to prevail IN ORDER for your retirement to succeed.

These do not, and can not, predict nor control world events, market conditions, your debts, taxes and other expenses, nor your choice of investment securities, etc.

Absolutely no guarantee is made nor implied, as to your actual outcome!

If you are new to this website, we recommend that you visit some of the links available at bottom of this posting,

providing more detailed information about our concepts and procedures.

One option used repeatedly in this posting, is the CUSTOM range calculation. You can use "Custom" to produce (Contribution, Yield) solutions in as narrow or as wide a range as you please. On the screen and just to the left of the "CALCULATE" button, you will see the text, "Contribution Range:" and then the word "Broad". Broad is the default option of a dropdown list. Click on this to show the list. "Custom" is the bottom-most choice. You'll be asked to provide values for two new data entry elements that will expand on the screen: a Central contribution value (your best guess of what you are looking for), and a Step value, which will increment additional contribution values above and below that central value.

Your choice of Range will appear in the title line of your on-screen results.

This, and other data entry items are explained in the on-screen HELP section on the right, the button labelled "What Else to ENTER".

Click here or scroll to bottom of this posting for links to all the HELP topics, as well as to the Calculator itself, and our other Articles.

To TOP of page

1: Broad-range Survey of Retirement Solutions using Fidelity's assumptions

Using NesteggCycle.com and working directly from the assumptions in the Fidelity article's footnotes ...Min Yield required for Broad Range Salary Contribs: 1 after contrib: yield is same PRE & POST Ret contrib: yield: sav/sal: withdrw: 2.50% 1 10.390% 4.995X 9.007% 5.00% 1 8.414% 5.985X 7.519% 10.00% 1 6.401% 7.348X 6.125% 20.00% 1 4.332% 9.293X 4.843% 40.00% 1 2.195% 12.185X 3.694% 80.00% 1 * 0.038% 16.514X 2.725% from MAX: 78.61% Multiplier of Salary & Prices during 42 working years: Salary: 5.0674 Prices: 2.7522 Spend_Power: 1.8412 PLOT EXTENDER IN EFFECT: Hi-C KEYPARMS_25_67_93_RPL45%_SAV0.00X_I2.5%_R4.0375%

Fidelity suggests contributions of 15%, so first we'll find the necessary investment yield to work with this.

Min Yield required for Custom_15_1 Range Salary Contribs: 1 after contrib: yield is same PRE & POST Ret contrib: yield: sav/sal: withdrw: 12.00% 1 5.863% 7.791X 5.776% 13.00% 1 5.625% 8.000X 5.625% 14.00% 1 5.405% 8.202X 5.488% -------------------------------------- 15.00% 1 5.198% 8.396X 5.360% -------------------------------------- 16.00% 1 5.005% 8.585X 5.242% 17.00% 1 4.823% 8.769X 5.132% 18.00% 1 4.651% 8.948X 5.030% 19.00% 1 4.488% 9.122X 4.933% KEYPARMS_25_67_93_RPL45%_SAV0.00X_I2.5%_R4.0375%

For Solution #2, let us find a suitable contribution amount that works with a yield of exactly 7.00%.

The initial report places this yield between the contributions of 5% and 10% so we'll focus between those values, truncating the outliers.

Min Yield required for Custom_7.5_0.25 Range Salary Contribs: 1 after contrib: yield is same PRE & POST Ret contrib: yield: sav/sal: withdrw: 7.50% 1 7.242% 6.725X 6.691% 7.75% 1 7.146% 6.791X 6.625% -------------------------------------- 8.00% 1 7.054% 6.857X 6.562% 8.25% 1 6.964% 6.921X 6.501% -------------------------------------- 8.50% 1 6.877% 6.985X 6.442% 8.75% 1 6.792% 7.047X 6.385% KEYPARMS_25_67_93_RPL45%_SAV0.00X_I2.5%_R4.0375%

Min Yield required for Custom_8.15_0.03 Range Salary Contribs: 1 after contrib: yield is same PRE & POST Ret contrib: yield: sav/sal: withdrw: 8.06% 1 7.032% 6.872X 6.547% 8.09% 1 7.021% 6.880X 6.540% -------------------------------------- 8.12% 1 7.010% 6.888X 6.532% 8.15% 1 6.999% 6.895X 6.525% 8.18% 1 6.989% 6.903X 6.518% -------------------------------------- 8.21% 1 6.978% 6.911X 6.511% 8.24% 1 6.967% 6.919X 6.503% KEYPARMS_25_67_93_RPL45%_SAV0.00X_I2.5%_R4.0375%

... and again ...

Solution #1 will be 15.0% contributions at 5.198% investment yield.

In the next section, for each of these solutions, we will work out the exact amounts accumulated at the ten year mark (age 35)

and compare with the benchmark of 2X salary.

To TOP of page

2: What it Will Actually Take to REACH 2X Salary Saved by Age 35

In this section, we will locate several pathways to 2X Salary Saved by Age 35.For starters, we need to determine what the age 35 salary will be, compared with the age 25 salary.

In ten years, we start with a first year at some initial salary, and get NINE (NOT ten!) raises.

Fidelity specified "real" raises of 1.5% per year. We have assumed inflation to be 2.5% per year.

The "real" raise is calculated as:

(1.00 + inflation/100) times (1.00 + raise/100) equals (1.00 + real_raise/100).

thus:

1.025 * 1.015 = 1.040375 ... giving a real raise of 4.0375% per year.

Nine such raises will multiply any initial salary by a factor of: 1.040375 to the 9-th power = 1.4279374

And therefore 2X the 10 year salary is twice the above: 2 * 1.4279374 = 2.8558748 times initial salary.

We need a suitable calculator which is capable of summing up the contributions, raises, and interest over some number of years (ten).

This savings calculator will do the job.

The starting salary amount is arbitrary. By selecting a power of 10 such as 100K, we simplify some of the math.

So let's make this concrete by assuming an age 25 salary of 100,000 per year.

Ten years later, this salary will have grown to 142,793.74 per year,

and twice THAT makes the 2X salary saved target value = 285,587.48

We must supply a contribution amount and an interest rate amount. Each time the "Calculate" button is clicked, the End Balance will be evaluated with the current set of inputs. If this End Balance is less than 285,587.48, we know that our combined contribution and interest rate are insufficient to achieve the 2X target in the ten years; if greater, we have exceeded the 2X target.

If we have a fixed contribution in mind, we can vary the input interest rates until we close in on a rate that brings us close enough to the target balance of 285,587.48; alternatively we can keep a desired interest rate fixed and vary the contribution until we close in on that same end balance.

What do we mean by "close enough"?

An end balance within about three dollars (2.855) is within one part in 100,000 of above 2X value. Solutions within a range of 5 times this, or about 15 dollars, are close enough for most purposes.

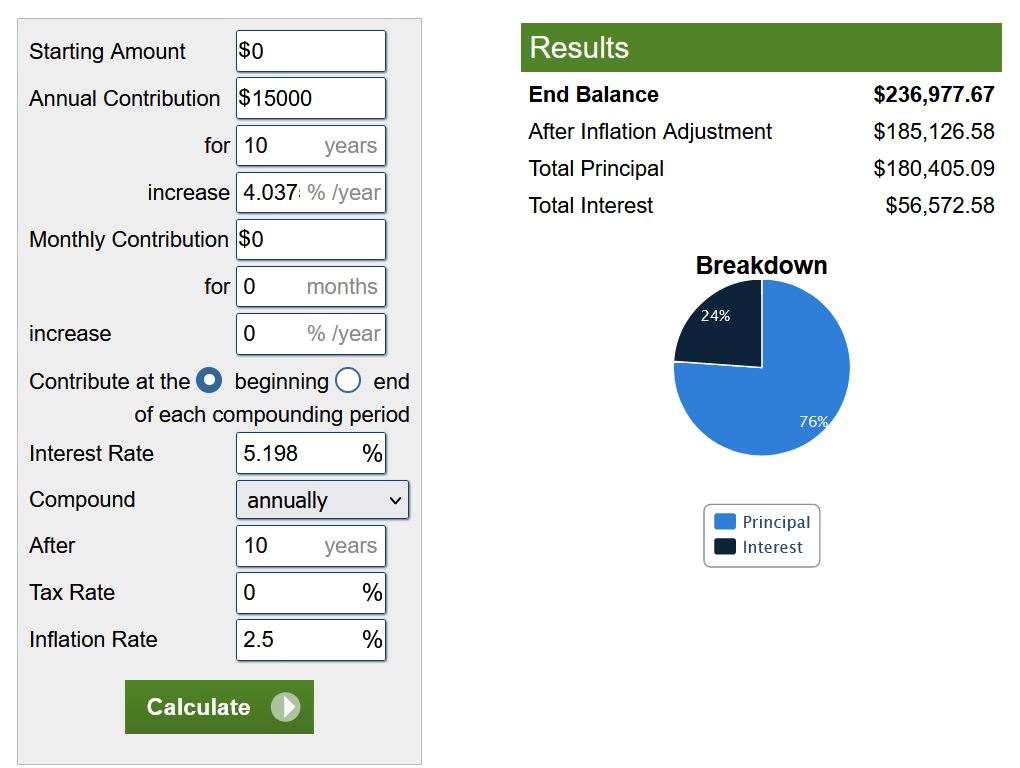

We'll start with Solution #1 as developed in Section #1:

Using the 15% contribution recommended by Fidelity, the retirement is satisfied at 5.198% investment yield.

Plugging Solution #1 into the savings calculator we get -- End Balance $236,977.67 -- 1.6596X salary, a little short of Fidelity's benchmark of 2X

For Solution #2 (8.15% contributions at 7.00% investment yield) -- End Balance is $141,753.67 -- only 0.9927X salary

Solution #1 asks the worker to do more of the heavy lifting;

Solution #2 asks the markets to do more of that! Therefore, market conditions permitting,

at a higher interest rate, you do not need as much money in the account to satisfy your retirement!

Since both fall short of 2X but Solution #1 comes closer,

we will use Solution #1 as the basis for a plan to calculate our first two pathways to 2X in ten years:

A: at 15.0% contribution ... raise the interest rate above 5.198% until we reach 2X

B: at 5.198% investment yield ... raise the contribution above 15.0% until we reach 2X.

THUS:

2X Solution A: at 15.0% contribution, required interest rate (yield) is 8.683%

2X Solution B: at 5.198% investment yield, required contribution is 18.077%.

We now seek a 2X Solution C which actually falls along Fidelity's retirement solution curve.

We know that the 15% contribution point provides LESS than 2X at ten years.

Recalling the original "Broad-range" solutions for Fidelity from Section #1, our next known contributions are

contrib: yield: sav/sal: withdrw: 20.00% 1 4.332% 9.293X 4.843% 40.00% 1 2.195% 12.185X 3.694% We calculate the 10 year savings for each, hoping to find a solution above 2X: 20.00% 4.332% ==> $301,783.38 ... IS OVER 2X 40.00% 2.195% ==> $539,323.67 ... IS MUCH OVER 2X

That is an estimated contribution of 18.75%. Are we getting close?

To find this out, we run a CUSTOM-range NesteggCycle.com calculation centered on 18.75% with steps of 0.10% to provide new points to feed into the 10 year savings calculation. The outliers have been truncated.

Min Yield required for Custom_18.75_0.1 Range Salary Contribs: 1 after contrib: yield is same PRE & POST Ret contrib: yield: sav/sal: withdrw: 18.55% 1 4.560% 9.044X 4.976% 18.65% 1 4.544% 9.062X 4.966% -------------------------------------- 18.75% 1 4.528% 9.079X 4.957% -------------------------------------- 18.85% 1 4.512% 9.096X 4.947% 18.95% 1 4.496% 9.114X 4.938% KEYPARMS_25_67_93_RPL45%_SAV0.00X_I2.5%_R4.0375%

The 10-year savings for (18.75%, 4.528%) is: $285,874.23, which is a few hundred OVER 2X, so YES, we are quite close but need to go a little lower.

We'll try the next one down: (18.65%, 4.544%); 10-year savings is: $284,590.76, about 1000 UNDER 2X.

2X Solution C will be closer to 18.75 than to 18.65, and works out to (18.727%, 4.532%)

This combination, 18.727% contribution at 4.532% yield, is the only result that BOTH satisfies Fidelity's assumptions AND achieves a ten year savings of exactly 2X salary.

Now we'll try to find some better ways to get to 2X.

In the same savings calculator session, we'll now look for off-the-curve combinations of contribution and yield which work to bring the 10-year sum to 2X, which again, amounts to 285,587.48.

We retain the raises of 4.0375%, the term of 10 years, and the starting sum of zero. We can reasonably take a little investment risk while very young. So let's try to find 2X solutions at yields of 7.00%, 8.00% and 9.00% ... we will play with the contribution until it gives us an End Balance within a few dollars of 285,587.48

Now that the process has been illustrated in detail, we will simply present the answers:

For 7.00% interest: contribution to reach 2X in ten years: 16.420%

For 8.00% interest: contribution to reach 2X in ten years: 15.561%

For 9.00% interest: contribution to reach 2X in ten years: 14.745%

Could we push even harder and go for saving 3X, 4X, or even more in ten years?

Now that we have the 2X calculations for 7, 8 and 9 percent, we can scale these up or down easily.

The required contributions will be in proportion to the desired end balance, at each interest rate,

so we have for 1X, half the 2X contribution; for 4X, double the 2X contribution, etc:

1X 2X 3X 4X 6X 8X

Rate

7.00% 8.210% 16.420% 24.630% 32.840% 49.260% 65.680%

8.00% 7.781% 15.561% 23.342% 31.122% 46.683% 62.244%

9.00% 7.373% 14.745% 22.118% 29.490% 44.235% 58.980%

However, there are organizations of people interested in "FI/RE" -- Financial Independence / Retire Early, who actively seek out such solutions. For those interested, one introductory article is here: Nerdwallet: Guide to the FIRE Movement

To TOP of page

3: Why you MIGHT WANT to save 2X Salary OR MORE by Age 35,

Why you MIGHT NOT NEED TO,

and Why the 2X milestone for age-35 is essentially meaningless!

Why you MIGHT WANT to have 2X Salary Saved by Age 35:

Any and all monies you can accumulate early into your career, translates into more options later on. This is because early money has more years ahead, in which to compound and grow. Therefore, it may become possible to increase your payouts, retire sooner, or "de-risk" your investments at retirement, by leaning extra-hard into early savings.

We will give some tantalizing hints of the possibilities here, with a more comprehensive discussion coming in Part2 .

with 2X saved by 35: age-62 retirement becomes possible at modest cost. with 3X saved by 35: age-62 retirement becomes very cheap! with 4X saved by 35: age-57 retirement becomes very cheap! with 6X saved by 35: age-47 retirement becomes very cheap! with 8X saved by 35: age-42 retirement becomes very cheap; age-37 retirement is possible at modest cost!

There are many ways to successfully achieve the Fidelity-specified retirement, in which the amount you have accumulated by age 35 will be less, possibly MUCH less, than twice your age-35 salary.

In fact, any solution using Fidelity's assumptions, AND with contribution UNDER 18.727% will have you under 2X yet perfectly on-track!

As long as you understand and are satisfied with these retirement goals, there is no reason to do more than just run the NesteggCycle calculation using Fidelity's assumptions but with your own current age and savings, and the CUSTOM Range centered on the actual contribution you are putting in, and verify whether the yield required to satisfy the retirement, agrees with the yield you are actually earning.

More on this, coming in Part2 .

Retirement solutions very much depend upon the assumptions you use!

In this posting, we've used a set of assumptions appearing in the footnotes of a Fidelity Investments article,

how-much-money-do-i-need-to-retire

You are urged to read and understand these, and to re-run the calculations with numbers more suitable to your own situation, your expectations for raises and inflation, your projected retirement lifestyle and expenses, and your projected other income sources, IF ANY, which might include for example: government pension, private pension, part-time job and/or side-business.

Fidelity assumed an end age of 93. At NesteggCycle.com, we routinely work with an end age of 105,and calculate payouts which will run the nestegg out of money after this age!

You might minimally want to re-run the calculations with an end age higher than 93.

And Finally to the CRUX: Why the 2X milestone for age-35 is Essentially Meaningless

In the table below, we have Solutions #1 and #2, and "2X Solution C", but have also added rows spanning a wide range of additional solutions:

Now THIS is interesting! The range of 10-year nestegg amounts (age 35) is a lot more extreme than the 42-year nestegg amounts! (age 67) contrib: yield: 10y sav: 42y sav: 42y/10y: 1.25% 12.344% 0.203X 4.254X 20.956 2.50% 10.390% 0.366X 4.995X 13.648 5.00% 8.414% 0.657X 5.985X 9.110 8.15% 6.999% 0.993X 6.895X 6.944 -- Solution #2 15.00% 5.198% 1.660X 8.396X 5.058 -- Solution #1 --------------------------------------------------- 18.727% 4.532% 2.000X 9.075X 4.538 -- 2X Solution C --------------------------------------------------- 25.00% 3.653% 2.549X 10.097X 3.961 40.00% 2.195% 3.777X 12.185X 3.226 60.00% 0.910% 5.298X 14.552X 2.747 75.00% 0.191% 6.380X 16.147X 2.531

Depending on the paired contribution amount and yield chosen for your solution, the above table demonstrates 31.4-fold variation in the 10-year savings/salary ratios, versus a more modest 3.8-fold ratio in the at-retirement (42-year) savings/salary ratios.

To review: each row of this table is a mathematically valid solution to Fidelity's posted retirement assumptions.

Each row will fund a retirement at age 67, with first year payouts of 45% of final year's salary, and 2.5% COLA's, continuing through age 93.

If the only thing you know at ten years is a savings/salary ratio, you truly do not know enough to track your progress!

To TOP of page

Basic site concepts:

NesteggCycle.com CONCEPTS

What This IS

What This Is NOT

Calculator Instructions:

Set Your GOAL

OTHER Entries

RUN it and FIND Your RESULTS

SPENDING POWER

Article Links, Calculator, and email address for your questions, comments and suggestions: