Nestegg Cycle © How to Stress Test your Portfolio

Posting Date: Mar.05, 2024 By: Fred P Davidson, Founder of NesteggCycle.comRev.A: Mar.19, 2024

Rev.B: Mar.25, 2024

Rev.C: May.08, 2024

Rev.D: Oct.29, 2024

Rev.E: Dec.19, 2024 -- SOLVER tools provided

Links to new CP "SOLVER" tools:

SOLVE_target_CP1_payout

SOLVE_target_CP2_reserve

INTRODUCTION: Concepts, Terms, and Assumptions related to this Stress Tester

To set the scene: It is 9:00AM on Day One of your retirement. Given your particulars ...

IF things were to go sour right now, just how bad could it get for your retirement?

This kind of bad news scenario happens to only about 20% of retirees,

and this calculator makes it simple to explore defensive alternatives.

For the luckier other 80% -- but you don't know beforehand which you'll be --

you would NOT need to deal with this, also known as Sequence of Returns Risk, or SRR.

Sections of This Posting -- Click to Toggle between

SHOWING

/

HIDDEN

Then scroll down to view the

SHOWING

Sections:

You provide five inputs:

Portfolio Yield, NET of inflation

YEARS Money needs to Last

Annual PAYOUT as PERCENT of your PRINCIPAL, your nestegg

Cash Reserve, and, Reserve Type

The Calculator

Calculated Stress Test Report: BEST viewed from Desktop or Laptop

where you can Resize by dragging lower right corner, JUST ABOVE.

On a PHONE, rotate to LANDSCAPE and use Height/Width buttons below for sizing.

Height: 10% - 20% - 40% - 80%

Width: 50% - 65% - 80% - 95%

DISCLAIMERS: This is just math. The calculations know NOTHING ELSE about your situation, other than the inputs requested here. Real-world markets can have unexpected complications. Please share these reports with a trusted financial advisor and do your own due diligence. We are not responsible for the performance of your investments.

We assume that during crash times, you are keeping up with inflation "somehow", possibly by moving the money to a money market fund.

This greatly simplifies the math, but you MUST keep this in mind as you consider these reports.

If you were NOT keeping pace with inflation, the crash results would be more severe than what's shown here.

The decision to DEPLOY these defensive measures, and to what extent, requires decisive action at the start of a crash, based on incomplete information!

This requires real-world wisdom which IS NOT, and CAN NOT, BE PROVIDED IN A CALCULATOR.

You would need to swing into managing your "worst expected scenario", immediately cutting your payouts from crashed equity, in accordance with these calculations, and for the number of years you specified.

This is a relatively RARE event: you may never need to deal with one.

Instructions for the Calculator

SEE ALSO: Main Discussion section, for additional insights; CALCULATOR section for Disclaimers.We assume, for purposes of the reporting, that your nestegg contains 1 million dollars.

This means that if you specify let's say, a 5.5% payout, the messages will show this as 55000 per year.

If you have for example 500,000, you would need to divide the reported dollar amounts by 2: 55000/2 is 27500.

Percentages and Crash-Points stay as-is.

This keeps your actual balance totally private because it never gets entered.

We have a somewhat specialized definition of a "crash":

It begins suddenly and completely on the morning of Day One of your retirement.

It is a synthetic construct, simpler than a real crash. A flat line, there is no jagged-line volatility.

This simplifies exploration of effects that might occur.

Our crash minimally means the LOSS of your net YIELD: You stop gaining against inflation.

This means we can have a "crash to 100%" at which you still have the whole million, but just no interest.

Indeed, this is the first situation we explore in each report.

A crash to 80%, for instance, would mean that the million suddenly dropped to 800000 in value, on Day One.

Our crash recovers suddenly, exactly on a retirement anniversary, by applying the inverse fraction to the remaining balance. So in the case of a crash to 80% (0.80), the balance remaining after payouts at end of the crash, gets multiplied by (1 / 0.80), which is 1.25.

After that, the portfolio yield (as entered by you) resumes immediately and until the end of the term.

We "crash test" your portfolio for periods of 2, 3, 4, and 5 years and report the outcomes for each crash.

Be aware that there is no "generic crash". Rather, the calculation depends on ALL the values you entered, as well as the duration of each crash, and its DEPTH. The depth of a crash is indicated as a "crash-to" percentage.

In our on-screen report, we show five "Crash To" depths for each crash length: 100%, 80%, 60%, 40% and 20%.

For each "Crash To" depth, we show how much of your payout can come out of crashed equity, how much (if any) needs to come from fixed income RESERVES instead, and the consequences of ignoring this distinction.

These consequences are shown in the "WHAT_IF1" and "WHAT_IF2" columns of the report.

Briefly: "WHAT_IF" numbers less than 1.00 tell you the fraction of your payout capacity that would remain.

Scroll down to the section, "Explaining the Report's Column Headers for each crash".

A Crash To 20% has not been seen since the Great Depression, which began in 1929, and ran through the 1930s.

Long-term Effects:

By this, we mean crash-related effects that spill over to the REST of your retirement,

depleting your nestegg to the point where the initially planned payouts can no longer be sustained through the planned end of your retirement term.

Your CRASH-POINT:

We have devised a measure of your portfolio's crash resistance, called its "crash-point", and by this measure, smaller is better.

Consider what happens if your portfolio's yield drops to zero for some years at the start of retirement, without losing any of its value.

You are retired and expecting to draw your payouts. How much will this affect you in the long run, if any? At low enough payouts, your nestegg may contain more than you actually require, providing some margin of safety. The crash-point tells you, for the particular crash in question, how much your portfolio could drop in value, and for how long, before you begin to suffer long term effects.

A crash-point value of 1.00 means that you are taking the exact maximum payout that will survive the "Crash to 100%" with no ill effects, but that as soon as your portfolio value were to drop at all, or you withdrew one dollar more than the planned annual amount, long term damage would begin. We flag as "BRITTLE", any crash scenario with a crash-point greater than 0.75, meaning that a sustained market drop of 25% leaves you susceptible to long term damage.

A crash-point value of 0.45, or even less, is a lot more desirable: your portfolio would need to crash down to 45% (450K on our hypothetical million, or less) before long term problems would set in.

The ages-old problem of "fear versus greed"!

Everybody would like the payout to be larger, and the risk to be smaller, but the tension is that these pull you in opposite directions, and so you need to experiment with alternative choices until you find something you can live with.

Assuming that your investment yield and time horizon are fixed, or nearly so, your main adjustment levers will be your Payout, your Reserves, and/or your Post-Crash Haircut.

Simplest for basic safety and security, is to reduce the annual payout until the results of a 3, 4, or 5 year crash look acceptable to you. Stay away from the Reserves and the Haircut for a first exploration, at least.

If you see that Reserves are needed at 100% or 80% or 60% crashes for 3 years, you are reaching for more payout than your portfolio can safely provide, and you need to step it down until it looks more reasonable. If you are depending on good crash protection at 4 and 5 years, apply this same screening process to those longer crashes, and yes, it will reduce the payout you can take.

In the following sections, Your RESERVE and Taking a POST-CRASH HAIRCUT

we describe the value proposition of this posting and calculator:

Some techniques you can explore to find more livable compromises between Payout and Crash-Resistance!

If you have other income sources such as a pension or Social Security which already cover your basic expenses, you may be comfortable farther out on the risk spectrum, seeking the better payout.

Your RESERVE -- "Add-On" or "Carve-Out":

We define your RESERVE as an additional pot of money, invested in a stable value account, like a bank account or money market fund, from which you can draw when your portfolio will not support your full payout. IF you are fortunate enough to HAVE such a fund, select "Add-On". The report will detail how much you would need to use it in the various crash scenarios.

IF you are not this fortunate, you will want to explore scenarios in which substantial market crashes will not impact your payouts. Necessarily, this will limit you to lower payouts, but it is vitally important to adhere to these limits if you cannot risk the shortfalls.

A new alternative: you can select the "Carve-Out" type of reserve.

This works WITHIN your original nestegg, but re-assigns a specified percentage of it to be your stable value reserve.

Even though this reduces the amount of assets earning the market investment yield, the extra stability does support larger payouts during a crash,

at a given level of crash resistance.

Taking a POST-CRASH HAIRCUT:

This is a trade-off you can try, but use this with CAUTION!

Effective with Revision C of this posting:

The Haircut is now treated as one more Reserve Type,

in the same drop down list as the Add-On and Carve-Out.

For additional information, select "Explain Reserve Type"

from the "Cash Reserve %" drop down list, and click the SUBMIT button.

Effective with Revision D of this posting:

A calculation error was discovered and fixed for the Haircut.

We see now, for the first time, that use of the Haircut is almost never a good idea.

The approximate "bang for the buck" ranges from about half, for very small increments close to the Crash-Point,

down to about one TENTH, if you are seeking serious crash protection, which is to say that

this approach can be TEN times as expensive, per unit of protection, as is the Add-On or Carve-Out.

Big CAUTION here: The Haircut reserve money has to come from somewhere,

and that somewhere is your FUTURE payouts AFTER the crash!

Originally conceived as a slightly more expensive option which allowed you to keep your whole nestegg invested, and worth the cost if you needed to use it, we now see this option more as an expensive last-ditch act of desperation.

This is so much less effective than the up-front stable value Reserve

because it consumes so much more of what would be your currently crashed funds, sharply reducing what remains when the markets recover; but it does offer simplicity, avoids up-front planning, and is one more option you can explore.

Don't worry if it takes you dozens of tries to reach a good compromise of Payout versus Crash-Point.

Each try takes mere seconds, and this is your retirement we're talking about!

Some EXAMPLES:

We typically look at retirement payout periods of 30 or 40 years, and long term investment yields around 7.0% above inflation, if you have nearly 100% equities in your portfolio. A 50/50 mix of stocks and bonds is a lot more stable, but drops your long term net yield to more like 4.0 to 5.0%.

You can enter whatever values suit your situation, but for perspective, we have pre-calculated some payouts that provide crash-points a little under 1.00.

EX1: PAYOUT 5.75%; YIELD 7%; TERM 40 years

This will stand up to a crash to 60% for 2 years, or 80% for 3 years, or 100% for 4 years.

In a 5 year crash, the crash-point is 1.125. and even at 100% portfolio value, we'd need to take 11.13% from reserves, or do without.

You need to make your own judgement call, as to how crash-safe you need to be.

EX2: PAYOUT 6.21%; YIELD 7%; TERM 30 years

This provides almost the exact same risk profile, but because we only need the money to last 30 years instead of 40 years here, we can take a 6.21% payout instead of 5.75%

EX3: PAYOUT 6.21%; YIELD 7%; TERM 40 years

This uses the same payout, 6.21%, as in EX2, but shows what happens if applied to the 40 year retirement.

With a crash-point of 0.68738, a 2 year crash here is safe down to 68.7%, which is fine, but only for 2 years.

In a "Crash to 100%", at 3 years, you'd need to take about 0.50% from reserves, and by 4 years, you must take 23.30% from reserves.

Author's Note:

These examples were developed early into this project, to illustrate that we can find different scenarios with similar Crash-Points.

All these weeks later, these now look far too risky, as the advice elsewhere in this posting, developed later, clearly shows.

If you run them now, you will see warnings that they are "Too BRITTLE!"

No reserves were explored in these examples, as the math had not yet been developed!

As an exercise for the reader, try re-working these examples until they conform to this posting's other advice.

Explaining the Report's Column Headers for each crash:

RESERVES to make up "n" year CRASH Shortfalls, Gentlest crash first:

Take from: Take from:

Crash To CRASHED EQUITY RESERVE RESV_as_%_of_Payout WHAT_IF1 WHAT_IF2

----------------------------------------------------------------------------------------

Crash To

The percentage of portfolio REMAINING at start of the crash

Take from CRASHED EQUITY

The dollar amount (on basis of a million dollar portfolio)

you could take from your crashed equity portfolio without incurring long term harm.

Take from RESERVE

The dollar amount (on basis of a million dollar portfolio)

you would need to take from fixed income reserves to complete your full payout,

or do without.

RESV_as_%_of_Payout

This normalizes the amount from reserve, as a percentage of the whole payout.

WHAT_IF1

Answer #1 to: "What if I take the whole amount from the crashed portfolio anyway?"

by showing the RATIO of (PRINCIPAL you'll HAVE) / (PRINCIPAL you'll NEED)

after the crash, toward sustaining your post crash payouts.

IF less than 1.00, you'll have to reduce your post-crash payouts by that proportion,

OTHERWISE you will run out of money too soon.

WHAT_IF2

Answer #2 to: "What if I take the whole amount from the crashed portfolio anyway?"

by showing the RATIO of

(YEARS you could have FULL payouts) divided by (YEARS you'll NEED PAYOUTS)

after the crash.

IF less than 1.00, you'll run out of money and have NO payouts in that proportion.

For example if you have 36 post-crash years and this number is 0.75,

your payments and money

will be GONE after 0.75 times 36 = 27 years.

IF greater than 1.00, you'd have more than enough through end of retirement term.

IF 999.9999, you'd have enough to get payouts FOREVER.

The Main Discussion

SEE ALSO: Calculator Instructions section, for additional insights; CALCULATOR section for Disclaimers.We hear it so often: What is a Safe Withdrawal Rate for spending from my retirement assets?

In this posting, we will look at the question differently.

The very short answer is: It depends!

We provide a new calculator, incorporating our new metric, the "Crash-Point", and use these to provide some surprising examples of exactly how and why the answer varies so widely, depending on the particulars of your situation.

The "Crash-Point" metric gives us a way to compare two retirement scenarios for crash-resistance.

Using this calculator, we have a way to engineer an abstract portfolio to a specified degree of crash-resistance.

We only run the crash tests up to 5 years, not longer, based on earlier studies that suggest that 3, or possibly 4 years, is the longest period on record with sustained deep cuts in equity value. SEE our earlier paper,

Stretching the 4 pct Rule which includes the historical reference to Bill Bengen's work.

We show you how to pull some levers you probably did not even know you had, to help you defend against Sequence of Returns Risk (SRR) while also enhancing your annual payouts.

Your CRASH-POINT:

We have devised a new measure of your portfolio's crash resistance, called its "crash-point", and by this measure, smaller is better.

Consider what happens if your portfolio's yield drops to zero for some years at the start of retirement, without losing any of its value.

You are retired and expecting to draw your payouts. How much will this affect you in the long run, if any? At low enough payouts, your nestegg may contain more than you actually require, providing some margin of safety. The crash-point tells you, for the particular crash in question, how much your portfolio could drop in value before you begin to suffer long term effects.

A crash-point value of 1.00 means that you are taking the exact maximum payout that will survive the "Crash to 100%" with no ill effects, but that as soon as your portfolio value were to drop at all, or you withdrew one dollar more than the planned annual amount, long term damage would begin. We flag as "BRITTLE", any crash scenario with a crash-point greater than 0.75, meaning that a sustained market drop of 25% leaves you susceptible to long term damage.

A crash-point value of 0.45, for example, provides a lot more leeway: your portfolio would need to crash down to 45% (450K on our hypothetical million) before long term problems would set in.

A crash-point value ABOVE 1.00 means that you would be taking more than your portfolio can support during the "Crash to 100%".

This is a dangerous place to be, since it means that even a period of mild market underperformance could be causing long-term damage without your even suspecting it!

Deriving The CRASH-POINT Formula (Part 1 - Primary):

We begin by observing that at the END of a crash, which began on Day One of retirement and recovered exactly "N" years later, we will require enough money to sustain our desired annual payouts through all the remaining years we planned. If our planned retirement term is "T" years, the post-crash money must last for T - N years.

To help keep this concrete, suppose T is 40 years, and our proposed crash runs for 3 years (N = 3)

So our post-crash time, T - N, is 37 years.

There is a well known annuity formula for finding the sum of money required:

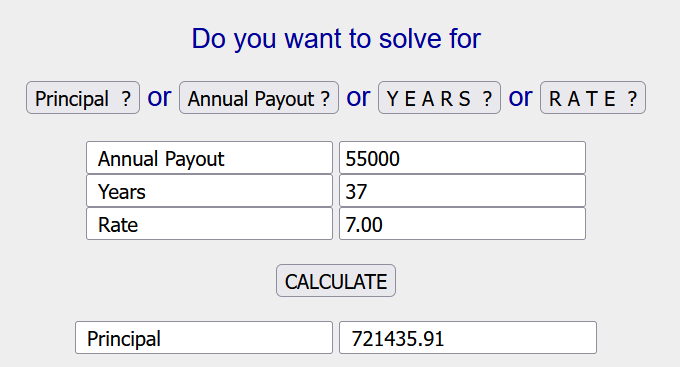

We provide the period of years the money needs to last (here, 37);

The expected Yield (net of inflation) which we will assume to be 7.00% per year;

The annual payout we want, and let's say for illustration, that we want $55,000 per year.

Plugging these values into the calculator at www.1728.org/annupay.htm and solving for PRINCIPAL, we get: 721435.91

For our calculations, we assume a starting value of 1 million dollars,

on which we'd want an annual payout rate of 5.5% to provide 55000 per year.

That gives us an "in-crash budget" of 1,000,000 - 721,435.91 = 278,564.09

for payouts DURING the 3 years of the crash. We NEED 55000 per year for 3 years, thus 165000, to get through this, and we have more than that, namely the 278,564.09 just mentioned. So far, so good.

But now imagine that your portfolio suddenly drops BY 60% in value, TO 40% OF its original value, from 1000K to 400K.

What can we say about getting paid our 55000/yr through 3 crashed years if this happens?

We need to end up with 721435.91, but we are starting with only 400K now so this looks completely unworkable.

HOWEVER ...

Recall that we just crashed to 40%. So PROVIDED THAT the recovery occurs on schedule, we only need to end up with

the crashed version of 721435.91, namely 40% of that amount: 288574.36

This looks more promising. We have 400000. We must end up with 288574.36.

The difference, 111425.64 is our in-crash budget for the three years.

Dividing by 3, we can pay 37141.88 per year.

It is a painful 3 years, but we are able to reverse the crash with our remaining 288574.36 multiplied by 1 / 0.40 ...

1 / 0.40 = 2.5; We recover to: 2.5 * 288574.36 = 721435.90 -- just enough to resume payouts of 55000/yr for 37 years.

[ Ideally, we would seek to make up the crash-time shortfall of almost $18,000/yr via sufficient Reserves,

otherwise we would need to do without. ]

Having seen these moving parts in action, the more interesting question is:

How can we find the borderline, crashed conditions

under which this portfolio can just barely pay the 55000 during and after the crash?

Knowing as we now do, that we need to come out of the 3 year crash with 721435.91 to handle the remaining 37 years,

our starting million could pay as much as 1000000 - 721435.91 = 278564.09 during the initial 3 years, while at 100% value.

That divided by 3 means we could have taken as much as 92854.70 per year during those three years!

How do we "scale this down" to a crashed situation which can pay exactly our 165000 (3 times 55000) and then RECOVER to exactly 721435.90, so that we live happily ever after? The answer is:

Total in-crash PAYOUT DESIRED ... the asked-for 165000: 3 years of 55000

divided by

Total in-crash PAYOUT POSSIBLE at 100%

... the 278564.09 as constrained by need to sustain payouts for remaining 37 years

THUS:

165000 / 278564.09 = 0.59232330 ... Crash to about 59.23233% (or, 592323.30 from our million)

How can we prove this?

1 - We crash to 592323.30, then pay out 165000 over 3 years, leaving: 427323.30

2 - Our RECOVERY is the exact INVERSE of the CRASH: We multiply the end-of-crash amount by 1 / 0.59232330

3 - 1 / 0.59232330 = 1.68826720

4 - 1.68826720 times 427323.30 = 721435.91 ... a perfect match to the amount we will need for the post-crash period!

This result, the fraction 0.59232330 or the percentage 59.232 is a CRASH-POINT.

It is THE (primary) crash-point with respect to a 3 year crash on a portfolio earning 7.00%,

and paying out 5.5% per year for 40 years.

It is the point at which, if the portfolio dropped to even a single dollar less,

AND if you tried to maintain the 5.5% payouts during the 3 year crash, damage to long-term payout capacity would begin.

IF the crash were to be any deeper than this value (here, rounded to 0.59232) the retiree has an important decision to make:

1 - Take the full payouts anyway, during the crash, and understand there will be a price later;

That price is detailed in the WHAT_IF1 and WHAT_IF2 columns of the report,

which are explained in the "Calculator Instructions" section.

2 - Heed the report's warning as to how much of the payment can come from crashed equity, versus how much from "RESERVES";

If you HAVE access to other funds (your RESERVE) elsewhere, use these to make up the rest of the payment;

OTHERWISE, endure the hardship of NOT TAKING that portion of your payout during the crash,

to preserve and sustain your long-term post-crash payout capacity.

3 - Work with the other levers we provide: Reserves or Haircuts, to free-up additional funds during the crash, but always at a price!

Now let us take a step back and look at the whole report, and observe that our 3 year crash protection is NOT very good;

We could survive a 3 year sustained market drop of about 41% (to 59.232%) but we'd want to survive drops to 40%, 30%, possibly 20%

And as desirable as the extra protection may be, we need to decide if we can afford it:

Inevitably this would involve some combination of reduced payouts (less than 5.5%) and/or provision of some reserves, or a "post-crash haircut".

Our protection at 4 years, the 4 year crash-point is weaker than that: 0.77721, meaning that long-term damage starts earlier, with our million crashed down to 777,210 or less;

And if we are concerned about a 5 year crash, that crash-point is 0.95527: long-term damage starts below 955270.

This is seriously deficient, since such a small drop is within the normal variability (volatility) of any market investment, and could mean damage where you are not imagining that anything is even wrong!

Please scroll down to Tables 1, 2 and 3 below.

Table 1 surveys the cost of achieving various low crash-points, corresponding to stronger crash protection.

To achieve the sort of protections mentioned just above, by ONLY adjusting the payouts,

we need to accept a 3.5564% payout to get the 3 yr crash protection down to 20%.

That's almost 20000/yr less pay than the 55000 we were planning for!

In Tables 2 and 3, we examine how provision of RESERVES can win back SOME of that paycheck.

To be conservative, we assume that you do NOT have additional funds to use as reserves, so we CARVE-OUT some of the principal to serve as stable, fixed-income reserves instead. One of the most interesting findings from the research behind this posting, was that this maneuver can buy back significant portions of payout, at constant safety.

From Table 3, a very solid compromise emerges, with 10% RESV carved-out, and payout% of 4.63545%, for an actual payout of 42140.45 from the reduced principal. The column to its right, with RESV of 20%, offers a paycheck of 47620.83/yr, but MUCH of that extra pay is coming out of the RESV money, even at modest crash levels where you do NOT expect to see that happening. This can work, but it makes life more complicated because you may need to manage your payouts to include money from the Reserve, even during periods of sub-par growth.

Exercise for the Reader:

Explore what happens at Reserves greater than 20%.

Can you achieve a 55,000/year PAYOUT at some higher carved-out Reserve, while staying with 7.00% investment yield, AND staying with the 40 year retirement Term, AND the "5 year crash to 32.958%" crash-point?

Deriving The CRASH-POINT Formula (Part 2 - Secondary):

This accounts for the protective effect of a given amount of fixed income Reserve money, by subtracting the Reserve from the desired payout, thus shrinking the numerator. If the reserves are greater than the payout, the minimum result will be set to ZERO.

(Total in-crash PAYOUT DESIRED) minus (Total RESERVES)

divided by

Total in-crash PAYOUT POSSIBLE at 100%

This does not negate the importance of the Primary Crash-Point!

You want to first get to a reasonable Primary crash-point, and THEN add some protection with Reserves, to a good secondary crash-point.

Otherwise, all you have is a poor compromise, dressed up to look pretty:

PRETENDING to pay yourself more, BUT really, you are dipping more heavily into the extra Reserves you have provided.

The degree of safety you require, depends on your personal circumstances:

If this is the money you depend upon for food and rent, you must maximize safety, as best you can!

But if basic expenses are covered elsewhere and this nestegg is for optional extras, you can accept higher crash-points (less safety) in exchange for higher payouts.

Wrap-Up:

IF you arrive at retirement with NO fixed income reserves, it might be worthwhile to sell a small fraction of your nestegg and invest THAT into fixed income. With a stable value reserve equal to (ballpark of) ten percent of your investable assets, you can get a surprisingly strong, steadying, amount of crash resistance.

One size does NOT fit all! Plug your own numbers into this calculator and explore what would work for you.

Especially after any crash, or excessive expenditure, or consumption of reserves, or period of market underperformance ... This calculation should be re-run!

Do NOT get complacent and assume that just because you and your portfolio have survived your first 5, 10, or even 20 years of retirement, that all is well. Years of slight overspending or slight market underperformance could leave you more vulnerable than you realize.

THUS, our strong recommendation is to run this calculator every year, keep long-term records of your crash-points, and make any adjustments needed to keep those crash-points trending DOWN!

TABLES:

TABLE 1: PAYOUTS for various Levels of Crash Protection (All: 40 years / 7.00% yield / ZERO RESERVE): PROTECT to CRASHPOINT PAYOUT --------------------- --------- 2 yr / to 30% 5.0351% 2 yr / to 20% 4.3114% 3 yr / to 40% 4.8501% 3 yr / to 30% 4.3256% ---------------------------------------- 3 yr / to 20% 3.5564% ---------------------------------------- 4 yr / to 40% 4.3411% 4 yr / to 30% 3.7923% 4 yr / to 20% 3.0271%

TABLE 2: Close-Up of cost of protection to "3 yr crash to 20%" Extra reserves bring the safe payout UP, even though they are carved out of the principal! RESERVE: 0% 5% 10% 20% PAYOUT(%) 3.5564% 4.4455% 5.3347% 7.1131% PAYOUT($) 35564.00 42338.10 48497.27 59275.83 4 yr: to 26.5% to 30.4% to 37.2% to 100%* 5 yr: to 32.9% to 40.6% to 53.9% to 100%* The protection is excellent for a "3 year crash to 20%" in each case, but watch what happens to longer crashes as the RESERVE and PAYOUT crank up: They don't scale up in the same proportions! 4 & 5 year crash protections get progressively WORSE at the higher reserves and payouts that maintain "3 year crash to 20%" protection in each case. (*) In fact, at the 7.1131% payout possible with 20% reserve, these 4 and 5 year crash protections are TERRIBLE, not even able to cover the relatively benign "Crash to 100%".

TABLE 3: Close-Up of cost of protection to "5 yr crash to 32.958%" Extra reserves bring the safe payout UP, even though they are carved out of the principal! RESERVE: 0% 5% 10% 20% PAYOUT(%) 3.5564% 4.0959% 4.63545 5.7145% PAYOUT($) 35564.00 39008.57 42140.45 47620.83 3 yr: to 20.0% to 15.7% to 10.0% to 0.0% 4 yr: to 26.5% to 24.4% to 21.6% to 11.2% 5 yr: to 32.9% to 32.9% to 32.9% to 32.9% Here, we start at 0% RESERVE with the same protection and payout as in Table 2, but this time we hold the 5 year protections constant at "Crash to 32.9%" as we move to higher RESERVES. This now provides stronger protections for 3 and 4 year crashes (compared with Table 2) but at higher cost, in the form of a lower ANNUAL PAYOUT.

To TOP of page